Steve FletcherâÄôs Northeast Minneapolis home is sandwiched between two foreclosed houses.

For him, like most Twin Cities residents, the foreclosure crisis has been more than a series of headlines.

But new data bears good news. Foreclosure sales in Minnesota for July, August and September dropped 32 percent from the same time last year, according to numbers released Friday by HousingLink , a Minneapolis-based group that gathers housing data.

Minneapolis is part of a national trend of rising home foreclosures and falling homeownership rates that hit the market more than four years ago.

The city projects less than 2,000 foreclosures this year âÄî a 33 percent decline from the peak year, 2008, when about 3,000 Minneapolis homes were foreclosed.

Some of the stateâÄôs highest foreclosure rates are in the north and south-central neighborhoods of Minneapolis. Unemployment and under-employment are among the largest factors for foreclosure sales in the state.

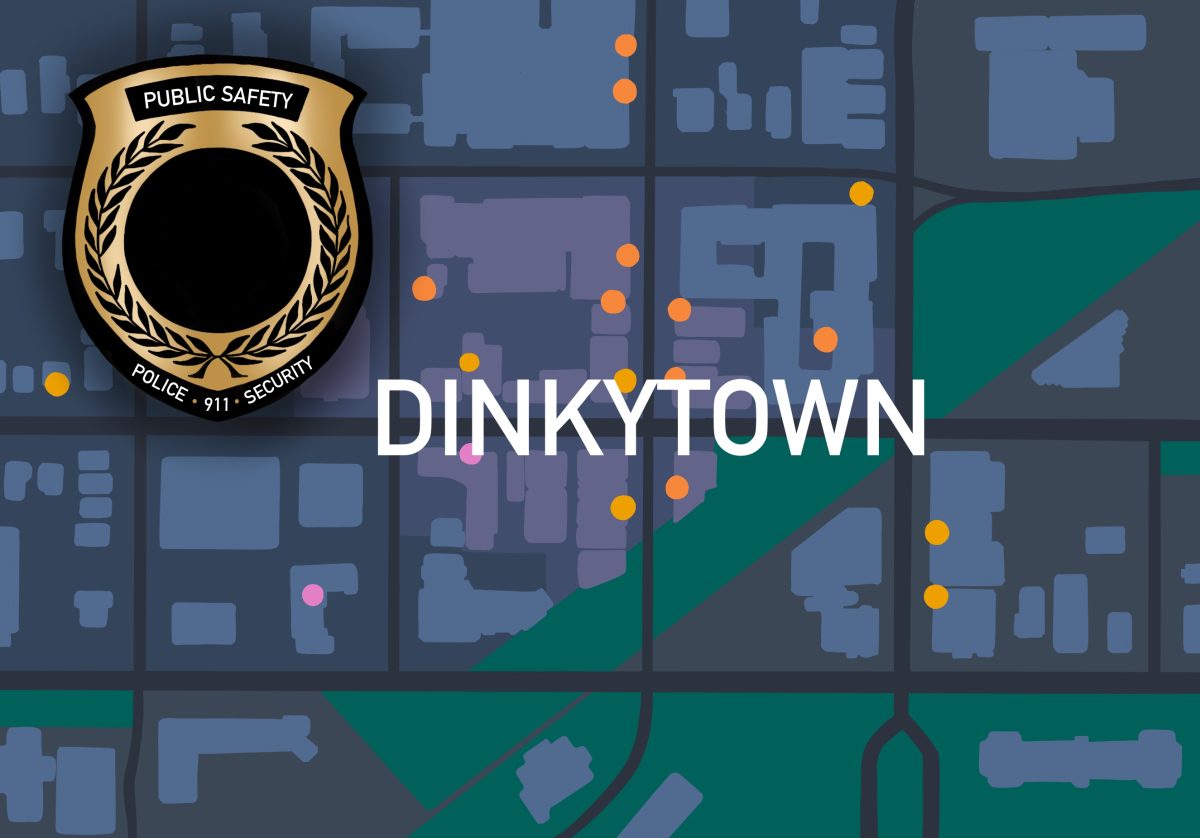

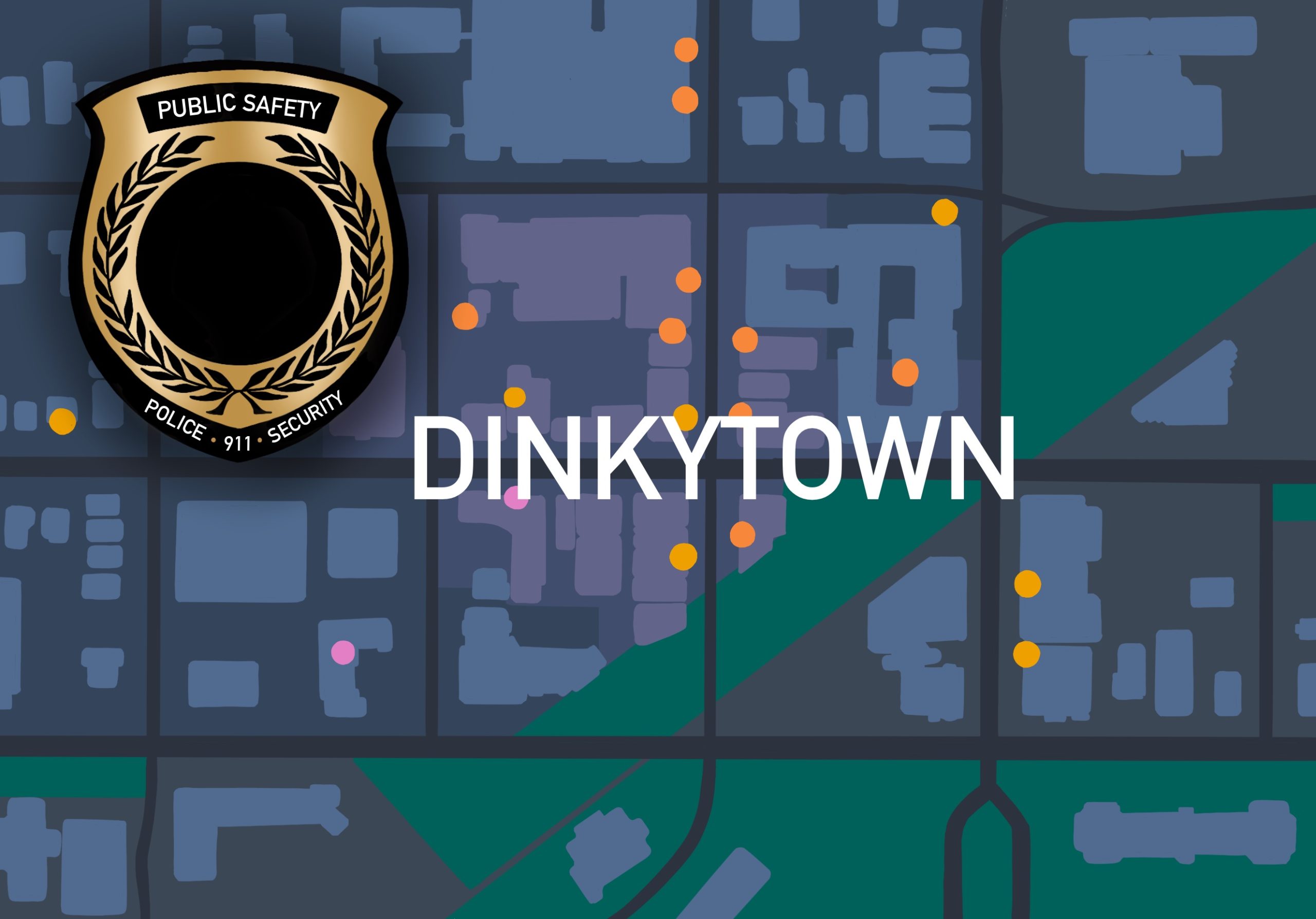

Meanwhile, University of Minnesota neighborhoods like Marcy-Holmes, Prospect Park and Southeast Como have historically seen fewer foreclosure sales because of their renter-based market, said Cherie Shoquist, the cityâÄôs foreclosure recovery coordinator.

According to the Hennepin County Sheriff OfficeâÄôs foreclosure database, Marcy-Holmes had only 11 foreclosures in 2010. There were 25 foreclosure sales in Cedar-Riverside, Prospect Park and Southeast Como last year.

As of September, the areaâÄôs foreclosure sales this year total about 18, according to Hennepin County data.

Before 2007, there were roughly 5,000 and 6,000 foreclosures in Minnesota per year. Numbers have since increased about 400 percent, said Julie Gugin, executive director of the Minnesota Home Ownership Center .

Bankruptcy attorney Ian Ball pointed to past practices of lending and borrowing, which added to the number of foreclosure sales in the state. Temporary financing was given to people who sometimes couldnâÄôt afford their homes, he said, making it nearly impossible for some homeowners to pay off their mortgages.

âÄúThere are a lot of consumers who unfortunately got in over their heads, and there was a lending industry that helped them jump into the deep end of the pool,âÄù he said. âÄúSome can swim, and a lot couldnâÄôt.âÄù

Gugin said the organization saw more instances relating to those practices when the foreclosure crisis first hit in 2007.

âÄúOver time, the foreclosure crisis that originated in the urban core has moved out to these areas,âÄù she said.

Although Hennepin County still has the highest number of foreclosures in the state, neighboring counties âÄî including Dakota and Scott âÄî have also been hit by foreclosures and short sales in recent years.

Data shows that Dakota County had 451 foreclosures in the third quarter âÄî a 27 percent decrease compared to the same period last year.

The Minnesota Home Ownership Center works with about 45 foreclosure agencies across the state, offering homeowners services like foreclosure prevention and refinance counseling. It will serve about 11,000 Minnesotans facing foreclosure sales or mortgage concerns this year.

Fletcher said many foreclosed homeowners are forced to relocate outside the city, which âÄúbreaks down the social network of a neighborhood.âÄù

âÄúWhether youâÄôre someone who can make their payments or someone whoâÄôs never had a mortgage, itâÄôs hurting everyone,âÄù said Fletcher, who is also the executive director at Minnesota Neighborhoods Organizing for Change.

The organization has targeted big banks, including Wells Fargo and U.S. Bank, for much of the blame.

But Ball said while lending practices capitalized on the average homeowner in recent years, it is something the market has seen before âÄî a housing bubble inthe early 1980s made more Americans into homeowners than ever before.

âÄúThereâÄôs a lot of finger pointing going around,âÄù he said. âÄúSure, the banks and mortgage lenders had a significant role in encouraging homeowners to take out loans âĦ but you also need a borrower to make a loan.âÄù